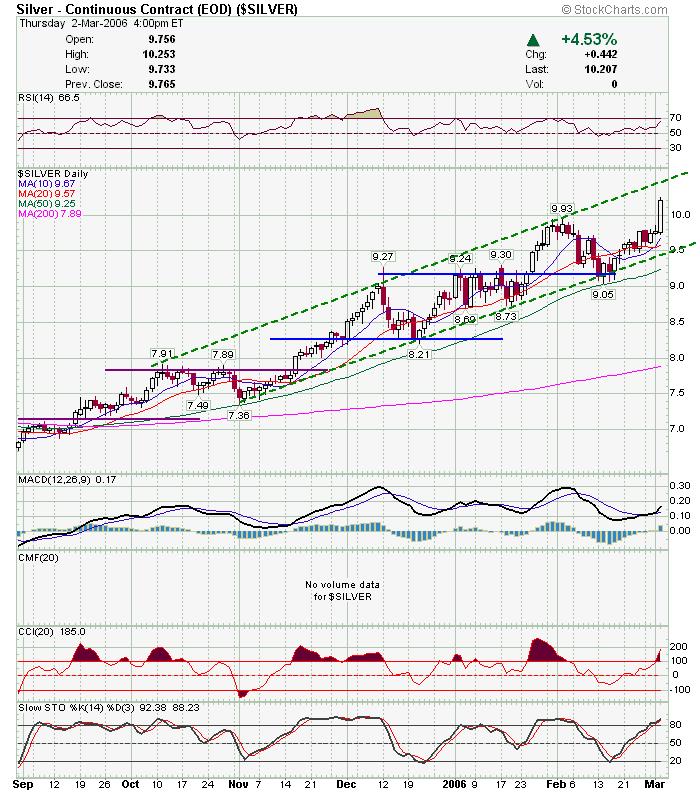

There was a nice move in all metal commodities as I expected today. Silver was the big winner today and it looks like it will head higher from here. I don't have much time tonight as I'm charting and playing poker at same time. I'm thinking Aluminum and Basic materials may get a little move next.

Here is the silver chart. I can envision silver trading to top of channel and possibly going over it short term. Here is SLW which I have recommended since below 5. Might be extended here, but with silver running you never know.

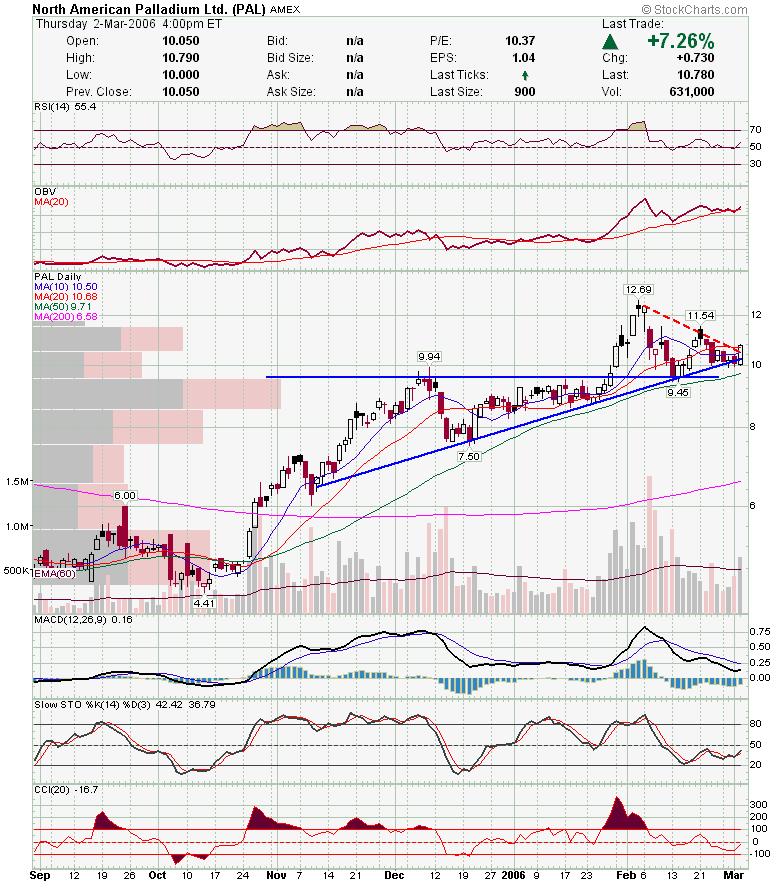

Here is SLW which I have recommended since below 5. Might be extended here, but with silver running you never know. PAL is a good candidate for a breakout.

PAL is a good candidate for a breakout. Oil has gotten a little move lately and still has room, but I think it may stall here.

Oil has gotten a little move lately and still has room, but I think it may stall here. Nice move here for CMT.

Nice move here for CMT. DLB just broke resistance and has room in the channel.

DLB just broke resistance and has room in the channel. SLB looks good here.

SLB looks good here. NTAP will push through resistance if Nasdaq makes a move up.

NTAP will push through resistance if Nasdaq makes a move up. AKS is forming a nice bull flag here.

AKS is forming a nice bull flag here. AL looks like it has bottomed here.

AL looks like it has bottomed here.

Good Luck,

DT

I imagine MACD crossed over on GLD ETF today and gold stocks are running like I thought they would. Take a look at GG, NEM, RGLD, and GLG for swing entries. Also, silver and copper is hot. I initiated a stake in PCU and PAL this morning, in addition to my current stake in SLW, GG, and NEM. Good Luck and please do your own DD.

DT

Gold has been going up and most gold stocks have been falling. I'm not sure why this is happening, but I don't expect it to continue. Looking at the past divergences haven't lasted too long, so I expect either gold stocks to turn up, or a deeper correction in gold to occur. For now, I 'm playing for gold stocks to turn up. Here is my gold stock of choice. They are the only one that has been going up steadily with gold. I believe the reason for this is Goldcorp's exposure to silver with the stake in SLW (my favored silver play along with svm.to).

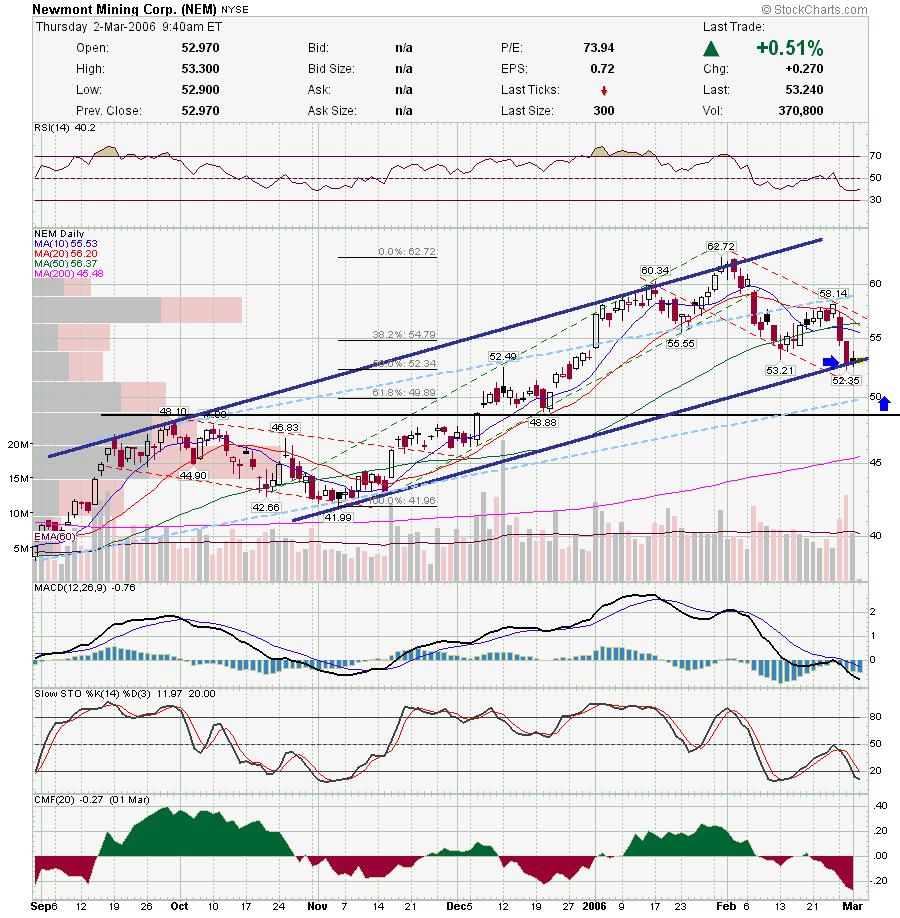

Here is my gold stock of choice. They are the only one that has been going up steadily with gold. I believe the reason for this is Goldcorp's exposure to silver with the stake in SLW (my favored silver play along with svm.to). Here is NEM's chart, and you can clearly see it pulling back. Looks like we have a possible bounce point here, or if it breaks a little further below.

Here is NEM's chart, and you can clearly see it pulling back. Looks like we have a possible bounce point here, or if it breaks a little further below.

Good Luck,

DT

Here is another great analysis from BTUFF. This is his review of BOOM's earnings report and SNPE's filing. Be sure to read my regular post from last night. I will also try and post my thoughts on gold later today.

Estimates vs. Actuals for Q4 2005

Starting at the top, revenues for the quarter increased 16% year-over-year (“YoY”) and 14% sequentially to $22.167 million. While my estimates were a little low on the explosive division and high on the AMK division, the differences offset and my overall estimate was off by only $67k.

While I was happy to see explosive revenues increase 17% YoY, I was somewhat disappointed with the flat AMK revenue. Management attributed the flat revenue growth at AMK to late-stage design modifications on the GE H System. These design modifications were cited as the reason behind the lower sequential revenue growth for AMK in Q3 vs. Q2. In the Q3 press release, these modifications were said to have been resolved but it was not clear if they were resolved at the end of the year or at the time of the report, which was more than a month into the fourth quarter. As such, it is highly likely that the same design changes that management discussed in Q3 had a continued impact on Q4. I want to ask investors relations (“IR”) about the design changes but I think these types of delays are to be expected during the early stage of work on the H System. Depending on my conversation with IR, I will probably carry my estimate of $1.6 million in AMK revenue over to the next quarter. I would imagine that GE will assume the cost of the design changes but that’s another question for IR.

Pre-tax margins were slightly below my estimate of 23.19% but up from 21.39% last quarter and 14.61% in the year-ago quarter. The actual pre-tax margin was 22.64%. All margins (gross, operating and net) have been increasing over the past year, including this last quarter, as a result of BOOM’s high fixed cost structure and management’s effectiveness in controlling expenses despite the company’s rapid growth. With the combination of higher sales and increased margins, income before taxes increased 80% over the year-ago quarter.

Finally, my overestimate in pre-tax margin was offset by my overestimate in the tax rate. My tax rate was 35% based on management guidance but I did say I thought this number could come in lower. The actual tax rate was 34%. In the future, I will continue to use a tax range of 34% to 37% unless management guides otherwise.

So….putting it all in a blender, my overestimates and underestimates washed out to a difference of $25k between my net income estimate of $3.482 million ($.28/share) and actual net income $3.457 million ($.28/share). Actual earnings were up 51% YoY and 10% sequentially.

Notes from the Report

The financial performance of the quarter was very strong especially when compared to the year-ago quarter, which benefited from the Ravensthorpe contract and miscellaneous tax benefits that resulted in an extremely low average tax rate of just over 21%. Furthermore, the year-ago quarter was the first quarter that started to bear the fruits of management’s restructuring efforts. I was impressed that BOOM was able to increase net income 51% despite these factors.

Aside from the financial performance, there were a lot of positives that came out from the earning release. For starters, the explosive division’s backlog increased 23% sequentially to $42 million; thus, indicating that demand remains very strong and getting stronger. The increase came despite the completion of New Caledonia and a large portion of Kuwait. While the $7 million contract for North American attributed to some of the increase, this was easily offset by the completion of the other big contracts. Where did the increase in the backlog come from? How many orders were booked in Q4? And, what was the average booking size? All questions I have for IR.

A second positive I took from the report is the planned increases in capital spending, which now includes a “major” expansion to the explosive facility in Mt. Braddock, PA. Previously management announced an expansion to the AMK facility in connection with the announcement of the supply agreement with GE. I would have to believe that management would not be planning the expansion to the explosive facility if they didn’t have good visibility into the future and didn’t see demand improving significantly over the next couple of years.

The budget for the planned expansion is more than the investment on the original facility. As construction costs have risen since the 1999 construction of the original facility, I would guess that the expansion will increase the footprint by 75% or so (total guesstimate and I didn’t crunch any numbers to come up with this). Lessons learned from the construction of the original facility, will result in the construction of a more efficient plant that will in turn likely increase capacity somewhere around 100%. Wait…I haven’t mentioned the big kicker to this…..management expects to fund the capital expansion through operational cash flow.

That brings me to my final point. Management is confident enough in the future cash flow of the company that they not only expect to fund the proposed capital expansion with cash but also feel comfortable enough to increase the dividend by 50% to $.15/share. The .4% dividend yield isn’t huge but does make the stock a little more attractive.

What Management Didn’t Say

One thing that wasn’t discussed in the earnings reports was the moderation of growth. Aside from the fact that it was already mentioned in the Q3 report, management likely didn’t say anything about moderation in growth because the coming quarter will show an increase in net income that once again hits triple digits. My expectation for triple digit growth in Q1 is based on my preliminary Q1 financial model and does not include the land put that should add about .12 to .13 to net income.

SNPE (Thanks to Smorg for brainstorming with me on the pros and cons of this)

SNPE is a French chemical company that owns just over 50% of BOOMs outstanding shares. SNPE acquired its position in BOOM through a combination of a stock purchase agreement, a conversion on its convertible debt holdings, and a private offering.

Mid-day yesterday, SNPE filed a 13D indicating that they were exploring the sale of up to all its shares (5,927,000 or 50% of total outstanding shares) in a secondary offering. Before we go any further, let me say that this is not a dilutive transaction because the shares held by SNPE are already outstanding. Furthermore, this is an SNPE transaction and BOOM will not directly incur any related expenses. I like the transaction because it will result in a road show that will increase BOOM’s exposure to the market, give management the opportunity to replace SNPE board members with new members, and bring control out of France and the French government and back to the US.

If SNPE relinquishes it shares to a number of investors, shareholders will have more control over the company. Greater shareholder control will make BOOM more attractive, especially to institutions. The lack of a controlling holder will also afford management the freedom to focus more on what is best for BOOM and on how to create shareholder value.

In addition to institutions, an offering to a number of investors may attract investment interest from customers (i.e. GE) and other corporations that see synergistic opportunities with BOOM. So long as these customers or companies are not taking a majority interest, this type of investor could be beneficial to BOOM by the way of contracts and supply agreements.

If SNPE was to sell all its shares to a single investor, that investor would be acquiring a controlling share and would likely be willing to pay a premium for the controlling share. While a premium would likely boost the perceived value of BOOM, we will want to carefully evaluate the investor in this situation. Nonetheless, a transaction of this sort would ultimately leave us substantially at the status quo.

If SNPE was to stumble across an investor that wanted both the SNPE shares and all of our shares, then we will have to go find a nice vacation spot where we can spend some of our gains.

If you look at SNPE’s financials, you will see a company with flat to declining sales, negative net income, declining cash flow and a deteriorating balance sheet. The sale of DMC is likely an effort to improve its balance sheet and return focus back to its core chemical business.

If you want an example of a similar transaction, take a look at AIZ. On January 21, 2005, a company called Fortis had an offering for more than 27 million shares that it owned in AIZ. Shares of AIZ closed at $30.6 on January 20, 2005. After the transaction, shares of AIZ trended higher and now trade above $45/share. That would be about 50% in less than a year. While the increase in share price at AIZ has likely been influenced by other factors, I think it is safe to say that the offering by Fortis did not impact the stock price negatively.

Strong move today for Nasdaq. Tech's led a charge today and it looks like several names are breaking out. Dow and SP500 lagged today and small cap volume wasn't all that great either. CSCO broke out today and I would look to FFIV, FDRY, and NTAP to possibly run tomorrow.

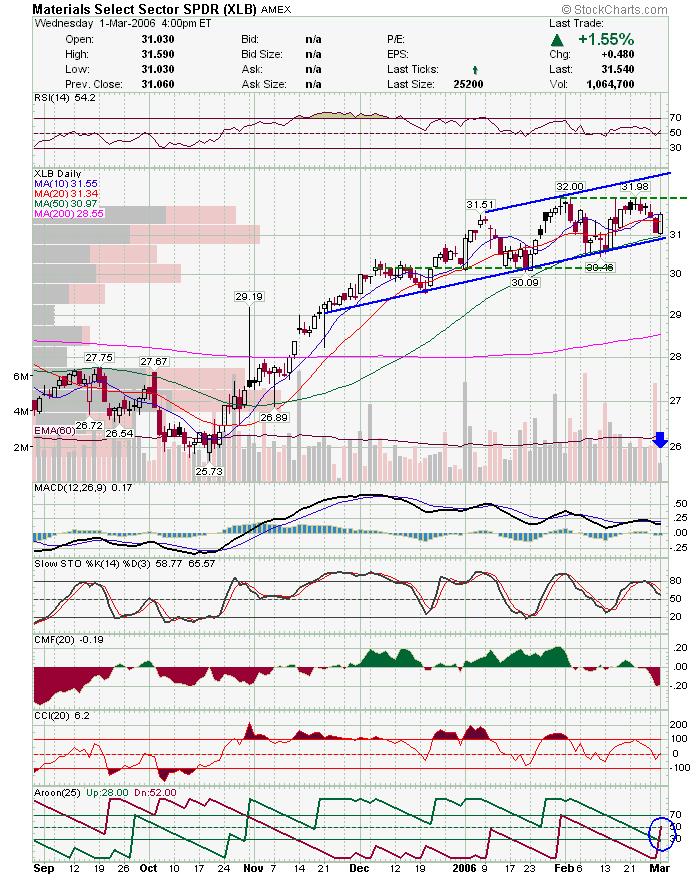

Basic materials look like they get a bounce up here off the trendline. Big warning here though as volume was pathetic. PCU looks like it will bounce here after copper's strong move today.

PCU looks like it will bounce here after copper's strong move today. CBST looks like it's breaking out here.

CBST looks like it's breaking out here. AKS may move if basic materials get the bounce.

AKS may move if basic materials get the bounce. JCP continues to show strength.

JCP continues to show strength.

AEOS reported earnings and management is really being rewarded for sticking by their company and buying up shares at 20. Cleared all sorts of resistance today. ENG testing trendline here.

ENG testing trendline here. HAL is at bottom of channel and showed a little strength.

HAL is at bottom of channel and showed a little strength. EZPW looks like a nice triangle break.

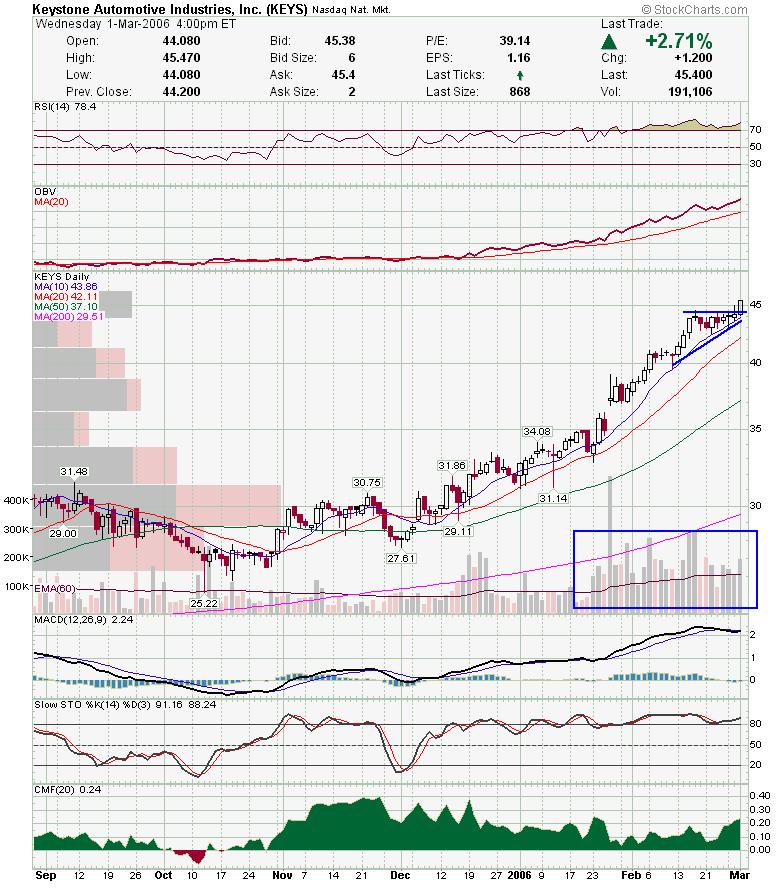

EZPW looks like a nice triangle break. KEYS is another triangle break.

KEYS is another triangle break. Big Triangle break here for MIDD.

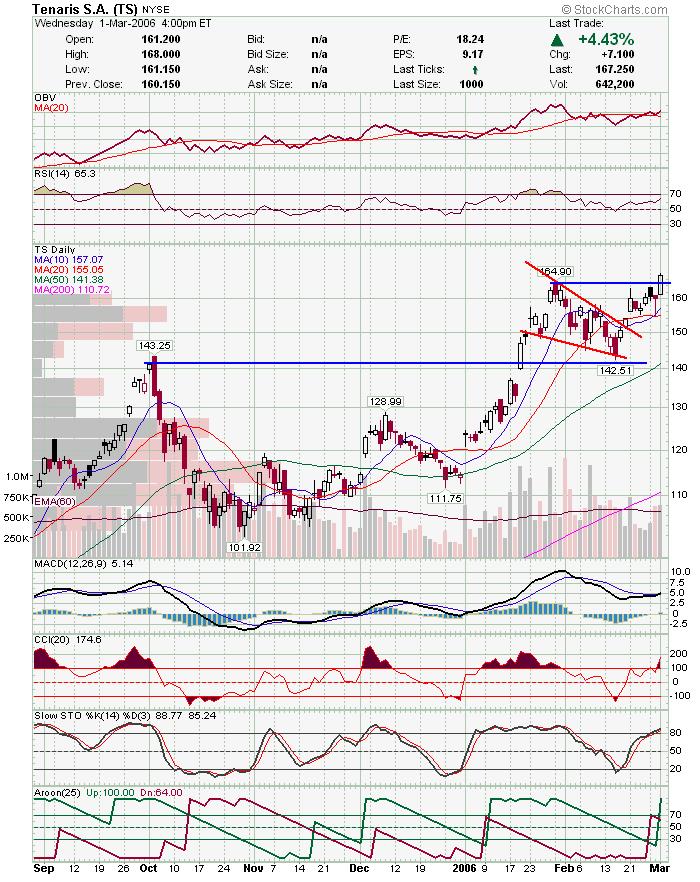

Big Triangle break here for MIDD. TS looks good here too.

TS looks good here too. Here is a short setup. LMS broke down yesterday and gapped up today and couldn't hold any of it.

Here is a short setup. LMS broke down yesterday and gapped up today and couldn't hold any of it. I was at the mall the other night and I passed by a Coldwater Creek store. The place was a cemetary. No one was in the store and I watched for a little while, and no one went in. Not one. Not that it means anything, but looking at the chart, CWTR broke down and then had a "Steve Nison" snap back rally, which has a target of the top of base that was broken. It hit target, and now looks like it will pull back. Keep an eye on it.

I was at the mall the other night and I passed by a Coldwater Creek store. The place was a cemetary. No one was in the store and I watched for a little while, and no one went in. Not one. Not that it means anything, but looking at the chart, CWTR broke down and then had a "Steve Nison" snap back rally, which has a target of the top of base that was broken. It hit target, and now looks like it will pull back. Keep an eye on it.

Good Luck,

DT

BCON released news of a successful test of it's flywheel system and is running over 30%. Keep an eye on it. It is up against resistance, but if it can break it, this could be a nice move. Please do your own DD.

Market internals look good today and several stocks are breaking out. I can't post charts from this PC, but CLB, INFA, ADAM, and JOYG are all at or near 52 week highs. Good Luck,

DT

Sorry, but I posted the wrong boom chart last night. I hadn't saved the one with yesterdays closing price. The updated one follows below. Good Luck,

Good Luck,

DT

GOOG got the blame for todays reversal, but the light volume leading up to the breakout hinted that the Nasdaq wasn't ready to run. Semi's haven't led this move and Nasdaq will go no where without semiconductors. SOX and SMH are still below resistance. I don't think the nail has been driven in the coffin yet but it looks like we have fallen back in to the wedge. You need to believe in your trendlines. Look at how BOOM has respected the trendlines that have been drawn well in advance. Watch for BOOM's next move.

You need to believe in your trendlines. Look at how BOOM has respected the trendlines that have been drawn well in advance. Watch for BOOM's next move. DRQ looks like it may head lower. Watch for support on recent pivot low, but if it fails, DRQ may head to 200 sma.

DRQ looks like it may head lower. Watch for support on recent pivot low, but if it fails, DRQ may head to 200 sma. Watch BHP here to see how it handles the current channels.

Watch BHP here to see how it handles the current channels. I was looking at GEOI as a possible long, but it's looking kinda shaky.

I was looking at GEOI as a possible long, but it's looking kinda shaky.

CTXS showed good relative strength today. JCOM may not even make it back to top of channel.

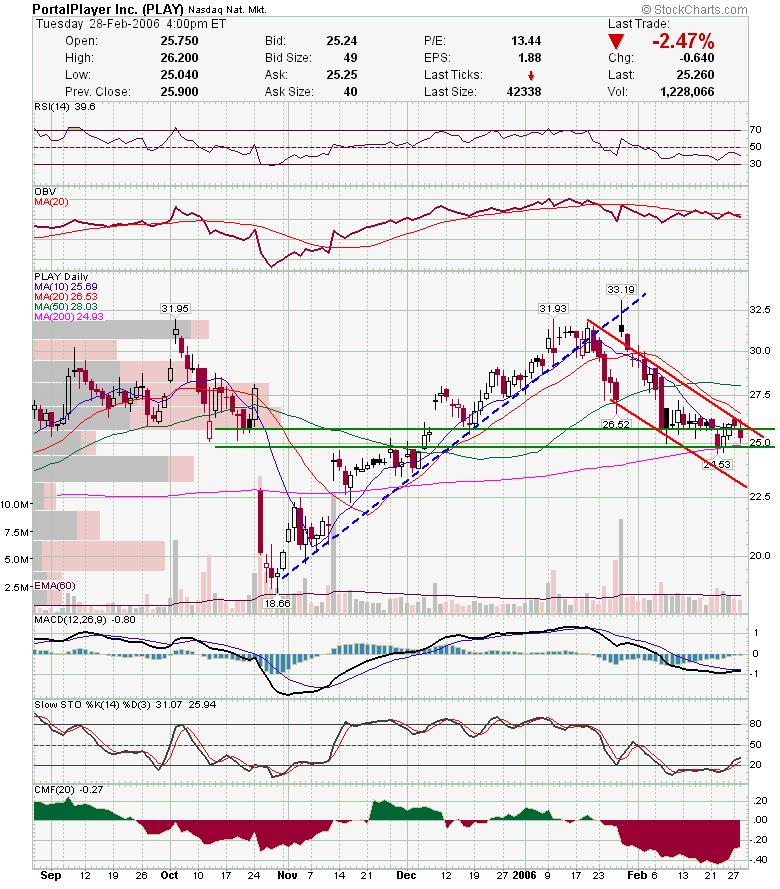

JCOM may not even make it back to top of channel. PLAY is suffering with the rotten AAPL. Watch for a break of the last pivot low.

PLAY is suffering with the rotten AAPL. Watch for a break of the last pivot low.

We are in a very choppy environment as I've mentioned a lot recently. I can't say for certain which way we are headed the next few days, but I can say that this is not the time to be getting aggresive. Good Trading,

DT

BOOM is trading higher this morning after reporting earnings. Here is my chart as of yesterday with the old comments left in. It looks like it will gap over the falling wedge and previous rising trendlines which should serve as support again. Good Luck to those trading it today.

Techs and Smallcaps led a rally today, however, as many are noting, volume was pretty ordinary. I am respecting the price action and support/resistance breaks, however, I am playing this move safer then I normally would. Lot's of what I've been posting the past few days has been looking good and some remain in decent entry points. Read back the past few days to look at the charts. Also, if anyone liked the post from btuff, let me know and I will harass him to start posting more regularly. It's different from my mostly technical viewpoint, but worthwhile reading in my opinion. Just a few charts tonight.

CMED may of bottomed out. The daily chart doesn't look all that impressive but they have reclaimed the trendline and will prob. test 50 sma in the next day or two. CMED Weekly looks better with it bouncing off a trendline and reclaiming the 10 week SMA.

CMED Weekly looks better with it bouncing off a trendline and reclaiming the 10 week SMA. TRCI action was weak today but held above previous resistance.

TRCI action was weak today but held above previous resistance. KLIC may get a bounce off the rising trendline here.

KLIC may get a bounce off the rising trendline here. CMT has been forming a nice contracting triangle.

CMT has been forming a nice contracting triangle. CTXS may of finally cleared this consolidation area.

CTXS may of finally cleared this consolidation area. ABAX had a strong breakout today on good volume.

ABAX had a strong breakout today on good volume. TRAD looks very good to me here. Volume was good and MACD looks like it will cross back over.

TRAD looks very good to me here. Volume was good and MACD looks like it will cross back over.

Good Luck,

DT

With BOOM reporting earnings tomorrow, my friend BTUFF thought it would be a good time to review 2005. BTUFF knows BOOM as well as anyone and a quick look at the yahoo BOOM public board will confirm this. His post follows below.

A Look Back at 2005

If there is one thing that is certain, BOOM is about to report nothing less than a phenomenal year for 2005. Assuming the one analyst following BOOM is correct in his estimates for the fourth quarter, BOOM will have increased sales for the full year 2005 by 44% and earnings by about 250%.

We entered 2005 with a backlog for the explosive division of $27.5 million. At the end of the third quarter, the backlog swelled to $34.1 million and that does not include the $7.5 million contract that was announced in December. Other major contracts during the year include the $5.3 million Goro Nickel contract announced in March and the $6 million Kuwait Olefins contract announced with the second quarter earnings report in August.

During the year, the AMK division, located in Windsor, CT, started ramping-up for work on both the GE H system and the expected increase in aircraft engine work. In December of 2005, AMK entered into a five year supply agreement with GE to perform a range of welding, heat treatment and non-destructive testing service on the H System. GE has announced planned installations of the H System in California and Japan. Based on my research, it seems to me that GE might be on the brink of a contract in Canada. It is interesting to note that one of GE’s F class turbines boasts the adoption of technology and materials developed from the H System. It remains to be seen if AMK will also be performing work on some F class turbines as well.

As for aircraft engine work, the company’s website lists all of the major aircraft engine makers as customers, except for Rolls-Royce (“RR”). While RR is not listed as a customer on the company’s website, RR was listed by management as customer in a 2005 press release. Both Boeing and Airbus announced record plane orders in 2005 and that should bode well for AMK.

In order to meet the expected demand for its AMK division, the company increased capital spending in 2005. This capital spending includes a new VAC AERO unit. Furthermore the company announced a “significant” expansion to its facility in Windsor to take place in 2006. After only three quarters, AMK has nearly matched revenues for all of 2004.

When comparing the first three quarters of 2005 with the full year 2004, gross profit margins have increased from 25.12% to 28.75%, operating margins have increased from 12.72% to 18.82%, and profit margins have increased from 8.13% to 12.32%.

Over the past year, cash flow from operations has been more than adequate to fund capital expenditures, eliminate almost all of the $3.2 million bank line-of-credit, and provide for modest pay down of long-term debt. Furthermore, the company arranged to convert $1.2 million, or 25%, of term debt to 200,000 shares. While cash and equivalents are down from $2.4 million to $1.8 million, I am more than happy with how the company has put the cash to work by paying down debt and increasing operational capacity. Despite the higher sales, accounts receivable have only increased modestly from $13.9 million to $14.1 million. Inventories have increased 50% and can be easily explained by the increased sales activity and expected delivery on the remaining Goro contract in the fourth quarter. With continued improvement to the balance sheet, the company declared a $0.20 annual dividend. My guess is that SNPE is behind the dividend.

Estimates for Q4

As BOOM reported exceptional results in the year-ago quarter, which included revenue from the $5 million Ravensthorpe contract and an exceptionally low average tax-rate of 24%, year-over-year comparisons will be far more difficult than the first three quarters of 2005. Nonetheless, BOOM has a few contracts up its sleeve. During Q4, the explosive division continued shipment on the Goro project and began shipment on the Kuwait Olefins project. I expect the AMK division to increase sales over both Q2 and Q3. AMK sales were down sequentially in Q3 because of late stage design changes to the H System. When the Q3 earnings were released, the design changes were completed and I suspect some of the Q3 revenue was pushed into Q4.

Given my expectations of 70% shipment on Goro, 30% shipment on Kuwait Olefins, and 65% shipment on miscellaneous backlog, I anticipate explosive revenue of $21.5 million for the explosive division.

With the continued ramp-up of the AMK division and my expectation that a majority of missed Q3 revenue will be captured in Q4, I anticipate AMK revenue of $1.6 million.

I expect the higher sales level in Q4 to boost margins but at a slower rate than the improvement of the past couple of quarters. I expect gross margins to increase to 32.5% and SG&A as a percent of sales to decrease to 9%. Subsequently, I get a pre-tax margin and pre-tax earnings of 23.19% and $5.36 million, respectively. At a pre-tax margin of 23.19%, the sequential improvement is half that of Q2 vs. Q3.

The company has guided for a full-year average tax bracket of 34%. A 35% tax rate for 2005 would need to accompany my analysis for a full-year tax rate of 34%. In my opinion, the tax rate is likely to be lower (i.e. 27.17% in Q3) but I will stick with my estimate of 35%.

Based on the above, I get $3.482 million in net income or $.28/share with my expected rate of dilution. This represents nearly a 52% increase in net income over the year-ago quarter and a 10.5% increase sequentially. For informational purposes, a tax rate similar to Q3 would yield a net income of $3.9 million or $.31/share. This represents nearly a 67% increase over the year-ago quarter and 23.76% sequentially.

The one analyst covering BOOM expects revenue of $22.06 million and an EPS of $.24/share. I anticipate BOOM to handily beat expectations but there is no saying how the market will react. Last quarter the year-over-year increase was in the triple digits. Will the market punish BOOM if net income increases only 52%? To me, that would be absurd but who knows when it comes to market reaction to earnings. With the high level of short-interest and a decrease in institutional ownership in the last quarter from 35% to 28%, it would appear that some market participants expect the price to go down.

As a sidebar, I think there is a 20% chance of some sort of secondary announcement to accompany the earning release. No science involved in this estimate, just a guess. Nonetheless, I have been tracking activity and project related to BOOM and I think the guesstimate is reasonable. Furthermore, it would not be the first time in 2005 that a BOOM earnings release was accompanied with some other good news.

A Look at Next Q

The first quarter 2006 earnings are bound to be strong. BOOM will recognize revenue on the remainder of the Kuwait Olefins contract and begin recognizing revenue on the $7.3 million North American refinery contract. I expect AMK will continue to show sequential improvement. As an added bonus, the land put that BOOM exercised in early January will add about $1.8 million pre-tax and about $.07 to $.08 to net income as a one-time item. Without the land put, I expect net income to return to triple digit increases when compared to the year-ago quarter.

The Next Few Years

According to Jim Rodgers, in his book Hot Commodities, the last three commodity bull markets have lasted about 17 years. The current bull market started in 1999. I believe we are now entering the point in the bull market where the wheels have been or are being put in motion to increase capacity. As such, I receive article after article from Google highlighting projects in the approval stages or in the bidding stage for the engineering, procurement and construction contracts. Given the explosive division is serving customers in the petroleum refining, chemical processing, hydrometallurgy, aluminum smelting, ship building, electrochemical, oil & gas, power generation, cryogenic processing, pulp & paper, and metal production industries, the outlook is seemingly favorable.

BOOM has a 60% global market share in explosive cladding. The only known competitors of BOOM’s explosive division are a Japanese firm, whose name escapes me, and some other much smaller firms. Furthermore, the process associated with BOOM’s “explosive” division has high barriers to entry given the nature of the process and the availability of explosive sites. While BOOM holds a commanding share of the market for explosive cladding, they do compete with other processes (i.e. rolled-bond) but it would appear that explosive cladding is increasingly being recognized as a superior process.

Good luck all,

Tuff

One of my stategies is to take a small percentage of my portfolio and allocate it to small caps with high momentum. I never use more then 4-5% of trading capital on any one of these stocks because they can be volatile due to the big spreads and small floats on some of these. But some of these end up being huge winners which more then makes up for the many failed trades. You need to be very strict with your stops as well, because a some of these end up falling hard when the trend fails. Here are a few on my current watchlist.

COGO has some powerful intraday moves and this is one that could make the IBD 100 if it makes it to 15. This one has decent financials behind it. ADAM looks like it will use previous resistance trendline as support in the near term. This is a motley fool tiny gem.

ADAM looks like it will use previous resistance trendline as support in the near term. This is a motley fool tiny gem. KLIC is another stock with strong IBD ratings.

KLIC is another stock with strong IBD ratings. SURG is basing in a bull flag.

SURG is basing in a bull flag. EGY is another one with high IBD ratings and has worked off it's overbought indicators.

EGY is another one with high IBD ratings and has worked off it's overbought indicators. TRCI is yet another one with strong IBD ratings. Looks like it tried to breakout and pulled back, but if it rallies again, it may hold.

TRCI is yet another one with strong IBD ratings. Looks like it tried to breakout and pulled back, but if it rallies again, it may hold. NICH looks like it has more room to run here.

NICH looks like it has more room to run here. Be sure to read my other updates from tonight below.

Be sure to read my other updates from tonight below.

Good Luck,

DT